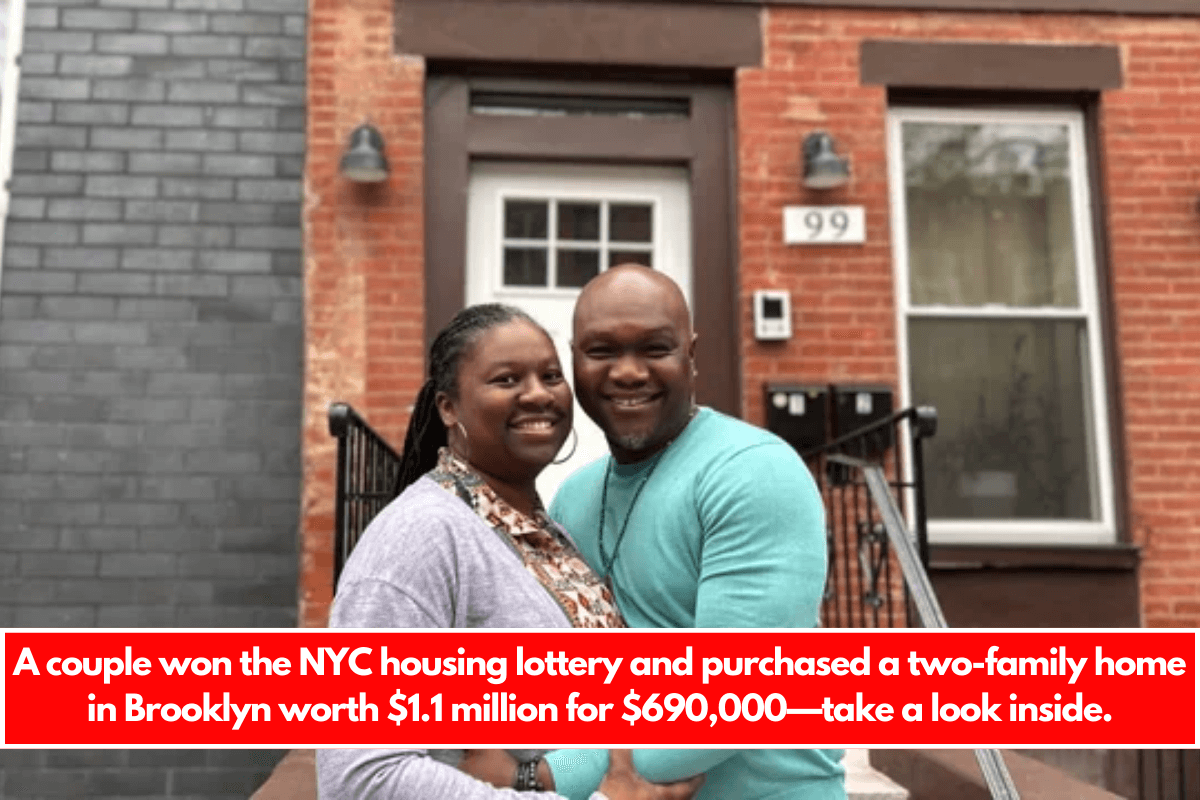

Tanese Orr and her husband, Robert Lashley, had been living in New York City’s public housing for nearly 20 years before Orr joined the city’s housing lottery.

“I applied for the homeownership aspect because I was already renting and didn’t want to leave an apartment for another apartment,” Orr shares with CNBC Make It.

Since 2015, the Small properties Rehab-NYCHA Program has facilitated the acquisition, rehabilitation, and sale of FHA-foreclosed properties owned by NYCHA to first-time homeowners.

Since 2015, 61 homes have been rehabilitated and sold to low and moderate income people.

In November 2022, three years after joining up, Orr went onto her Housing Connect profile and saw an active lottery for properties that the city was repairing.

Less than two months later, Orr received an email requesting that he provide a list of required documents, including pay stubs and bank account information for everyone in the home. They had only two weeks.

Following the submission of the application, the couple viewed two homes: a three-family house and a two-family house in Brooklyn’s Clinton Hill area.

According to Zillow, the average house value in Clinton Hill, NY is $971,984, a 2.2% increase over the year.

The objective for each of these properties was to keep them cheap and accessible to former NYCHA residents.

Orr was intimately familiar with Clinton Hill. She worked at a Blockbuster in the region in the early 2000s and recalls telling folks at the time that she planned to reside nearby one day.

“When I originally got the position I remember gazing around and saying ‘I really love this neighborhood and I want to live here,'” Orr recounts.” “At the time, I had no intention of buying anything.

I dropped out of high school, was a teen mom living in the projects, and worked at Blockbuster for the minimum salary at the time. I had no idea how I was going to do it, but I was confident it will happen for me. I can’t believe I’m living here now.”

Orr was initially interested in the three-family house, but the couple were outbid.

The two-family house has been totally remodeled and consisted of two sections. The second story had a one-bedroom, one-bathroom apartment, while the first floor had three bedrooms and one-and-a-half bathrooms. The house also included a backyard and a finished basement.

For the family, it was a reasonable second alternative. “We loved that it had a backyard,” Orr says.

Orr and her husband took for a $691,000 mortgage with a $36,369 down payment and $23,395 in closing charges. The house was worth $1.1 million, and the Department of Housing Preservation financed the remaining purchase price through a second mortgage. They also obtained a down payment assistance loan of $15,000.

The couple obtained a 30-year, low-interest rate mortgage from the State of New York Mortgage Agency at a rate of 6.6%. The monthly mortgage was $4,968.36 when they closed, but it has subsequently risen to $5,275.53, according to paperwork examined by CNBC Make It.

“People think that we just won the lottery and we got it for free but that’s not true,” Orr tells me. “We still had to have a good amount saved.”

Despite the fact that closing on the property took more than six months, Orr says she was determined to buy the two-family home at any cost.

“During the procedure, they [HPD] continued requesting for more documentation, but I didn’t mind. “I was going to figure out a way to get everything to them because I knew it would be my home,” she says.

Orr closed for the house in October and will relocate in November 2023. One of the conditions of purchasing the house through the NYC Department of Housing Preservation and Development was that the couple rent out the upstairs one-bedroom apartment. They identified a tenant who will move in October 2024 and pay $2,584 per month in rent.

The family has lived in the property for just over a year and says the most difficult adjustment has been getting used to all of the costs associated with owning rather than renting, such as paying for water, remembering to take out the garbage, and overall upkeep.

“We went from paying $1,800 a month to $5,000 a month for our mortgage. “It was an adjustment,” she admits.

Despite this, Orr believes it’s worthwhile now that she and her husband are homeowners.

“The best part is saying that it’s ours and saying we did this and we were responsible enough to save and work hard for this and it’s ours,” she tells me. “It’s a peace of mind.”

Because of that sense of pride, Orr says she doesn’t plan to sell the house, although she does want to buy another property in the future.

“I love Brooklyn, I love the neighborhood and I love that house,” she tells me.

Orr’s main piece of advise after going through the NYC housing lottery is to realize how important your credit score is. “Even if you have the money, if your credit is not right, you’re going to miss out on a great opportunity.”